consumption per capita in the U.S.

In the last few years the chicken industry endured major disruptions like the great recession and the great grain shortage and minor disruptions like trade disputes and bird flu issues. With all the turmoil, the possibility of having a great year seemed to be remote and in the far future.

Suddenly, however, the sun came out and the stars aligned. Grain prices are falling, chicken prices are strong and the competing meats are retreating from the playing field. This rising tide will lift all boats at least temporarily.

Good news starts with corn prices

The good news started with corn. After record high prices in the last few years, the world supply of corn finally caught up to demand and corn prices fell dramatically in this crop year 2013-14 with prospects for even lower prices next crop year. The bull market for corn, once juiced by rising ethanol production, is now being replaced by a bear market for corn assisted by relatively stable ethanol production.

Waiting on soybeans to catch up

The good news on grains will be complete when the price of soybean meal falls. Soybeans have been stubbornly resisting the gravitational pull of corn thanks to rapidly rising demand for soybeans in China and lingering effects of drought in South America. However, the inevitable crash was merely delayed not cancelled. The hot market for soybeans in China went off the boil just as soybean production accelerated across the world. By August, soybean meal should be $100 less per short ton than the peak price earlier in the year. The chicken industry is likely to find the cost of both corn and soybean meal unusually reasonable during crop year 2014-15 compared to the last several years.

Supply of competing meats lagging behind demand

A spell of low input costs would be cause enough for celebration, but when combined with a shortage of competing meats it creates the best of all possible worlds. Both beef and pork supplies are dropping this year providing a great opportunity for chicken.

The competing meats convert grain to meat less efficiently than chicken and were therefore affected to a greater degree by the combination of recession and high grain prices. In addition, because of the long life cycle of cattle, it takes years to change from declining production to increasing production. The beef industry is faced with highly favorable prices for beef but a biological inability to take advantage of the demand for at least another year or two.

The situation in pork is somewhat different. Pork production is more immediately responsive to changes in demand than beef but is hampered by disease problems this year. It is estimated that pork production will be at best the same in 2014 as it was in 2013 with a shortage of pork expected during the summer months.

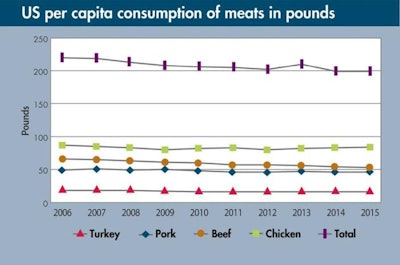

The current supply situation in meats is illustrated by the table of per capita consumption. The great recession resulted in a drop of 21 pounds of meat consumption per capita in the U.S. between 2006 and 2015. Beef is still falling while chicken is rising. The meat recession in the U.S. lasted for 10 years.

As good as it gets for chicken industry

As the supply of meat continued to fall recently the economy began to accelerate. While not perfect by any means, the U.S. economy is growing and unemployment is dropping. The demand for meat is increasing at a time when the supply is slow to respond. The result will be high prices until supply has a chance to catch up. It appears that it will be mid-2016 at the earliest when meat supplies are able to increase and prices begin to moderate.

This is as good as it gets for the chicken industry. Those who learn from history will shore up the balance sheet during these good times to be prepared for the next inevitable downturn.