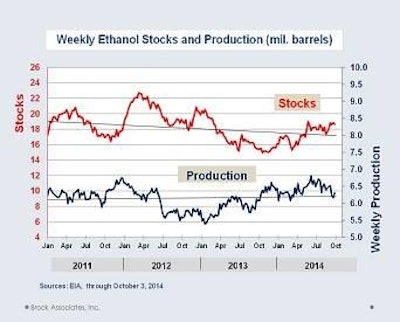

In my previous article for WATT readers, I mentioned the need for DDGS supplies to keep moving to eliminate their potential to weigh on corn prices. The latest data from the U.S Energy Information Administration (EIA) says ethanol stocks have slightly increased while production has diminished over the past few weeks. This is a key factor of market balance of supply and demand the industry follows very closely.

Over time, nearly all commodities experience the process of rebalancing to maintain consistency of supply and demand. For ethanol, there is more to it than that, such as adjusting to the seasonality of gasoline use and availability of feedstock. Since the Great Recession, we have also learned there is less elasticity of demand for gasoline when priced at greater than $4 per gallon. Rebalancing for certain commodities can occur quickly; it depends on the dynamics of that commodity whether the process takes weeks, months or even years. Regardless, the laws of economics will prevail and the market participants of that commodity eventually learn that lesson.

Timing is very important for success in the commodity world. The timing could be better right now for the ethanol industry if ethanol stocks were not so high at the same time a record corn harvest is available. We expect this imbalance of high ethanol stocks to be a short-term matter, but would not rule out a one- or two-month span to achieve a better balance.

Past production and stocks trends as seen from the chart included in this article should not be looked at as being highly reliable -- not just yet anyway. Keep in mind, the ethanol industry is still a fairly new industry that has gone through a lot of challenges such as a rapid growth, reduced feedstock supplies, a major recession, a trade partner for the key byproduct that is inconsistent, and competition from other countries that produce biofuels. We expect ethanol use of corn to be steady over the next year unless the export countries of Canada or Northern Europe step up their imports and take potentially extra volume the U.S. market does not need. It also needs to be pointed out that ethanol use of corn is roughly 75 percent of the total industrial use category of corn. Prior to ethanol’s existence, the other industrial use of corn was impacted by general economy trends, but not enough to weigh greatly to the price of corn. That is not the case now. The price of corn is now impacted by general economy factors as well as global market conditions.

In order for the ethanol industry to succeed, there is a degree of collaboration that is necessary within both the major producers and smaller producers. While the industry is competitive like any other industry, in order to maximize plant investments and returns, the industry needs to work together to achieve a favorable balance between production and stocks that drive a margin of profit.

Tim Brusnahan joined Brock Associates in 1985 and provides commodity price forecasting, research analysis, hedging and marketing strategies for crop producers, dairy and livestock producers and procurement/risk management strategies for feed manufactures, corn processors, and other end users. Contact Brusnahan at 414.540.2607 and [email protected].

The views and opinions expressed are not a solicitation of trading futures and options contracts. There is risk of losses as well as profits when trading futures and options, careful consideration to all risk aspects of commodity/derivative trading should be considered before trading, and past performance is no indication of future results.

.jpg?auto=format%2Ccompress&crop=faces&fit=crop&h=48&q=70&w=48)