A Dutch report that appeared at the end of 2009 has directed attention to organic pork production in the European Union. The organic sector remains only a small part of the total market for pork in Europe. Whether it can grow again, as consumer choice is restored after the current economic troubles, will depend on the price premium needed to cover the extra cost involved in its production.

At the LEI institute that forms part of the Wageningen University and Research Centre in the Netherlands, pig production economist and InterPig group member Robert Hoste has led an investigation into the costs of producing organic pork in the EU countries mainly associated with this sector – the UK, Germany, the Netherlands and Denmark.

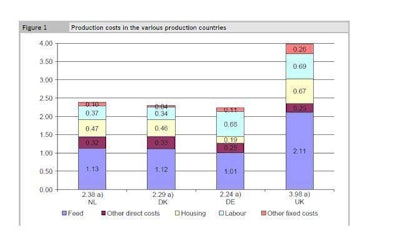

The results are summarized in the accompanying Figure 5.

Note that the figures are shown in Euros and that they refer to an assessment of

costs over a period from 2005 to 2007. The cost price of €2.38 per kilogram slaughter weight calculated for the Netherlands is indicated to have compared with €2.29 for Denmark, €2.24 for Germany and €3.98 for the UK.

By way of comparison, Pig International has reported previously on InterPig’s estimates in relation to standard pigs. These concluded that producing each kilogram of conventional pork in 2005 cost €1.23 in the Netherlands against €1.29 in Denmark, €1.45 in Germany and €1.53 for British units. In 2007 economists calculated Dutch costs to have moved higher to €1.47 per kilo, while the Danish average had become €1.40, Germany’s was almost €1.60 and Britain’s worked out at nearly €1.78.

So the implication, from setting these alongside the figures now available from the Dutch research, would seem to be that organic pork can cost at least an extra 40% to produce when compared with standard pigmeat and in the most extreme case may even have more than double the cost per kilogram.

High British feed prices and the relative disadvantages of outdoor production are quoted in the LEI report as explaining how the UK’s organic pork cost was above that of the other EU countries. Some other differences in cost are attributed partly to a gap in national figures for feed conversion, with the average Dutch whole-herd feed conversion given as 3.17 and that for Danish herds as 3.45, while comparable rates in Germany and the UK were put at 3.70.

The report says the indication of Germany having the lowest cost for organic pork reflected production on smaller farms in rather old housing. But it forecast that those producers would eventually leave the business. With the remaining units using newer and therefore more expensive houses, the effect would be to increase the overall German cost of production.

The question is then, which EU country has the costs structure to succeed as an supplier of organic pork to the biggest European markets for the product -- those in Germany and the UK? Robert Hoste and his colleagues point to an estimate that over half the quantity produced in the Netherlands between 2005 and 2008 was exported. The country also has the highest share of organic pork consumption, measured in meat turnover in the retail level, even if organic represented only about 1.9% of total meat sales in 2007.

Both the Dutch and the Danes are strongly export-oriented, says the LEI report, with highly productive primary sectors which produce at low costs. Compared with the Netherlands, the Danes have the advantage that they have a slightly lower cost price, more options to expand and a pig farming sector with a more natural image. But the Netherlands can still compete on costs due to its streamlined chain, in which production is co-ordinated and sales take place mainly through conventional retail channels.

What is more, the largest single player nationally is allied to one of Europe’s largest pork processors and so has good access to German and British outlets.