Poultry is the nimblest animal protein, and having adjusted more quickly than beef and pork to the slow-growth economy and biofuels era grain prices is now positioned to eat into the market share of beef and pork.

The next 12 months is poultry’s opportunity to capture market share from red meat competitors – especially beef – before those competitors swing to profitability and increase production, says Christopher Hurt, professor of agricultural economics, Purdue University.

Opportunity for chicken

“This is a long-term opportunity for the chicken industry,” Dr. Hurt said in a presentation at the Chicken Marketing Seminar. “The chicken industry is in position to quickly increase production and make money while the beef supply remains down.”

“Per capita supplies of animal proteins are going to be down for the next two years,” he said.

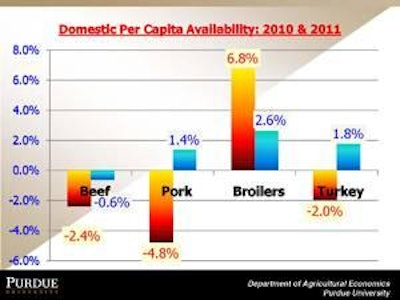

Per capita availability of meat and poultry

Poultry’s opportunity comes as the pork and beef industries continue to reel from the aftershocks of the recession in 2008-09 and the run-up in feed prices due to the diversion of corn to ethanol production. Both industries have suffered significant economic losses in the past two years as production costs exceeded revenues, and beef and pork production remains below 2006-07 levels.

Using 2006-07 as the baseline, Hurt projects that the domestic per capita availability of red meats and turkey will be down in 2010 – beef -2.4%, pork -4.8% and turkey -2.0%. Chicken availability, on the other hand, is expected to be up 6.8%.

There’s no sign that the beef supply is going to begin to rise in the next year, and any increases in the pork supply won’t begin to reach the market until the fourth quarter of 2011.

Meantime, retail prices for beef and pork will hit record highs this summer, Hurt predicted.

Corn prices limit profitable meat production

Hurt said corn prices will determine the limits to profitable production. He predicts that corn prices will range between $3.50 and $4.00 a bushel on average over the next several years.

“If corn prices stay under $4 a bushel, there could be a modest expansion of red meats on a profitable basis. But if red meat supply expands more than 2% to 3% over the next several years, that would put profitability in jeopardy.

“The animal proteins industries won’t be able to return to producing 220 pounds per capita of meat and poultry. The supply can be increased to 210 or 212 or 214 pounds but not much more in the biofuels era,” he said.

Biofuels policy to change diets worldwide

While the corn/feed price scenario of 2008 may not be repeated in the immediate future, U.S. policies favoring the use of corn for biofuel production over food production continue to shape the economic landscape for animal proteins.

“U.S. biofuels policy is going to change the composition of diets in the U.S. and around the world. We will have to look back later to know for sure, but we may be out of the 40-year period of overall increasing per capita consumption of animal proteins in the U.S.,” Hurt said.

Mature U.S. market saddled with biofuels

The U.S. market for animal proteins is a mature market and is not going to show much growth in the future – especially given corn/feed prices in the biofuels era, Hurt concluded. What’s more, U.S. meat and poultry producers face a challenging array of regulatory issues (see “10 challenges for animal proteins”).

“The U.S. animal proteins industries have made most of their adjustments to the big economic shocks of 2008-09. Now, while there’s a big domestic market, the future growth is in exports,” he said.