Download data:

Two charts reproduced here tell an important story in relation to the prospects of the global poultry market. One matches income to meat purchasing, the other demonstrates the rise in disposable incomes that is already occurring in the largest countries.

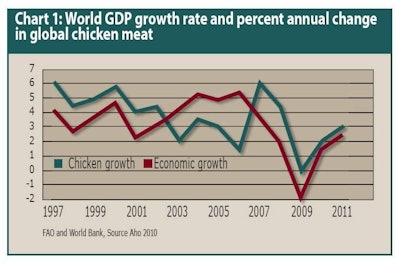

Chart 1, from a presentation in 2010 by Dr. Paul Aho and based on FAO and World Bank data, shows how closely the size of the world market for chicken has stayed in step with the strength or weakness of the global economy over the last 10 years.

Chart 2 is from the China Animal Agriculture Association, illustrating that 30 years of population growth in China was joined by a significant rise in personal incomes as more people moved from the countryside into towns and cities.

Higher rates of urbanization are developing quickly in many countries and are having a profound effect on buying power. Their impact was modified in 2008-09 by economic recession internationally, as expressed by negative growth in the Gross Domestic Product (GDP) that is used most widely to measure the economic activity of countries, regions or the world as a whole.

Recovery in GDP

Global GDP (which is calculated by valuing goods and services produced during a specified period of time) fell by 1.9% in 2009. However, economists at the international agencies projected a recovery starting in 2010 that would restore the annual rate of growth to around 3.3% by 2011.

The recovery would mean more buying power, which in turn translates into a stronger world meat market for two reasons. One is the habit of people in the richer countries of increasing their purchases of meat in total and of more expensive cuts of meat in particular. The other is the fact that income improvement in the developing countries brings more people to the point where they can afford to eat meat.

Chart 3, from IMF, also follows the progression of annual GDP changes over a period of five years. But it makes the point that the developed-economy nations of the world were affected more deeply than countries classified as emerging or developing. Even within this latter category there have been major differences in GDP change over time from one region or country to another, as Chart 4 shows. Although it might seem to suggest that regional economies will develop more in unison over the coming decade, Chart 5 from Australian agricultural economics bureau ABARE indicates a wider separation of patterns between regions.

More in Asia

Without a doubt it was Asia that made the strongest recovery from recession in terms of its regional GDP in 2010. Both domestic demand within Asian countries and sustained exports contributed to this resilience. For 2011 the rate of growth of Asia’s GDP has been forecast to come in the range of 6.5-7.0%. China might even manage 9.5%, the forecasters added, and India could achieve 8.5%. An Indian report said that poultry production in India could look forward to expanding due to the demand surge created by higher incomes and associated changes in eating habits. An expansion of 40% or more appeared possible by 2015.

In projecting an average GDP rise of 3.3% per year to 2019, analysts at the U.S. Department of Agriculture also pointed to the contribution likely from a number of other developing-economy countries and those of eastern Europe. Strong growth in emerging-market economies was already contributing significantly to the start of the global recovery seen in 2010, said OECD.

With the better demand from higher incomes should come an increase in the price of foods. Although less for chicken than for other meats, FAO identified a general strengthening of international meat prices from 2009 into 2010 and projected relatively firm price levels for poultry meat in the next 10 years.