WATT’s 2011 Poultry Nutrition and Feeding Survey shows a cautious industry, affected by the world grains crisis and energy costs, but with intentions of using more enzymes and dried distillers grains with solubles and investing in new equipment and facilities.

WATT PoultryUSA, Industria Avícola, Poultry International and Feed International magazines asked 224 industry people responsible for producing and using poultry feeds worldwide about their business outlook and key trends, involving composition of rations, sustainability, investment, use of enzymes and more. Here are the key findings:

- In terms of business outlook for this year, more than a third feels there will be an improvement over 2010, as compared to more than 50% last year.

- Economics and financial issues dominate the top five challenges. Once again, “cost of grains/volatility in grain prices” was ranked as the most important concern in all world regions, followed by “energy costs, including transportation and milling.”

- Feed production volume is predicted to increase from 2010 figures by more than half of respondents, just as poultry and egg production volume.

- To support these increases, companies are planning corresponding investments in feed equipment and facilities.

- The upward trend in the use of alternative feed ingredients, including DDGS and enzymes, continues.

Business outlook for 2011

Worldwide, the poultry nutrition sector’s business outlook is not as optimistic as it was in 2010. In terms of business outlook for 2011, more than a third (38.2%) feels there will be an improvement over 2010 – compared to more than 50% of last year’s perception. Almost a third (31.8%) foresees negative or deteriorating profitability in 2011 due to economic conditions, while almost another third (30%) sees no change in profitability from 2010. The business outlook is quite different among the world regions. For almost half of the U.S. respondents (47.6%) the outlook is for negative or deteriorating business conditions, while in the rest of the world only 28.2% of respondents had a negative business outlook.

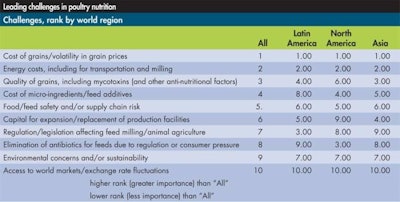

Major challenges in nutrition and feeding

Economics and financial issues were identified as among the top five challenges. Once again, “cost of grains/volatility in grain prices” was ranked as the most important concern in all world regions, followed by “energy costs, including transportation and milling.” “Quality of grains, including mycotoxins and other anti-nutritional factors” was rated third, followed by the “cost of micro-ingredients or feed additives” and “food/feed safety and/or supply chain risk” tied as the third most significant challenges. Respondents ranked “capital for expansion/replacement of production facilities” as the fifth most important challenge facing their operations.

Challenges of lesser importance

The three challenges ranked as less important by all world regions were “Elimination of antibiotics for feeds due to regulation or consumer pressure,” “Environmental concerns and/or sustainability” and “Access to world markets/exchange rate fluctuations.”

Composition of rations

Worldwide, the upward trend in the use of alternative feed ingredients, including DDGS and enzymes, continues, according to survey responses.

While 42.5% of respondents said “none is used now or in the past three years,” 38.6% indicated their use alternative ingredients had increased. Twenty-four percent said usage had “increased somewhat over the past three years” and 18.2% said usage had “increased significantly over the past three years.” Also, 18.8% said usage stayed the same over the past three years.” Interestingly, almost a third (29.4%) thinks usage “will increase somewhat,” and 10.6% believe usage “will increase significantly.” A quarter of respondents said usage “will stay the same” in the next 12 months.

In terms of enzyme usage, almost half (46.8%) of the respondents say it will increase from 2010 levels, while almost 38.7% say it will remain the same. So the overwhelming majority is giving the use of enzymes an important role in feed formulation. Two-thirds of respondents (62.2%) say that enzyme usage will increase over the next three years. Almost half of respondents (48%), however, expect that their phytase use will remain the same as 2010, while 34.5% say it will increase.

The primary objective of formulation continues to be the least cost per ton of finished feed for almost half (45.3%) of the survey worldwide participants – less in the U.S. (35.9%) than in the rest of the world (47.7%). Nonetheless, 37.6% formulate for least cost per live pound/kg of poultry. Some forward-thinking producers believe that other formulation objectives, such as least cost per ready-to-cook pound/kg of poultry or per pound/kg of further-processed products, must be followed, but in this survey those percentages are still negligible.

Marketing and labeling

There is no doubt labeling is increasingly important for poultry and egg products. Most of the respondents in this category make claims in their labels that their poultry, for example, is “all natural” or contains no hormones, no antibiotics/drugs, no animal by-products, among other claims. However, almost no one ties this to quality, such as HACCP or ISO, or the use of other enriching nutrients, such as omega 3.

Sustainability

More than half of respondents (52.4%) say their company has a written sustainability strategy, which includes nutrition and/or feeding.

Production and investment

More than half of respondents (51.4%) predict worldwide feed production volume to increase from 2010 figures, while a third (31.3%) thinks volume will stay the same. Only 17.3% believes it will decrease. Pretty much the same figures were obtained for the poultry/egg production volume, with 50%, 35.9% and 14.1%, respectively. However, in terms of poultry production, the U.S. is less optimistic, with 30.8% forecasting an increase in volume in 2011, compared to 57.4% in the rest of the world.

To support these increases, companies are planning corresponding investments in feed equipment and facilities, particularly replacement and upgrades to feed milling equipment. The same is also observed for poultry production facilities and equipment. In the U.S., three-quarters of the respondents believe investments will be in replacement/upgrading feed milling facilities and equipment, compared to 41.7% in the rest of the world.