Demands for cheap meat from austere yet welfare-conscious domestic consumers, soaring input costs, falling carcass sizes and depressed imports all make for an interesting time for UK producers. But all is not doom and gloom, according to the National Farmers Union.

The weakness of Sterling has had a major effect on trade by depressing imports but is only part of the picture. Brazil has failed to make use of its chicken meat import quota, blaming a change in UK law that prevents previously frozen meat to be sold as chilled.

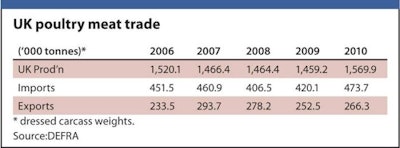

The local producer

Far from becoming a more global world, the recent financial crisis could be argued to have snapped some perspectives back to those before the advent of cheap air travel. The local producer is king in the eyes of today’s consumers, wishing to consider the carbon footprint of their Sunday roast whilst maintaining a firm grasp on their grocery budget. In truth, UK supermarkets have long been staunch supporters of UK producers. Virtually all fresh, whole chickens sold in supermarkets are already British so they were well ahead of the game.

In the first three months of 2011, UK poultry meat imports, exports and domestic production were little changed compared the same period in 2010. Imports were 111,500 metric tons and exports, 62,800 mt. Domestic production rose by just 1.3% to 379,700 mt (from 374,900 mt). Exports were virtually static at 62,800 mt (from 62,900 mt in 2010). However, exports should receive a boost thanks to China overturning its ban on UK poultry imports.

The preference for white meat among UK consumers has long created a carcass imbalance – with exports being predominantly of dark, leg meat and imports of breast meat. However, customers are looking for more affordability, especially if this can be achieved without sacrificing notions of animal welfare. To stick with key consumer price points, many supermarkets have reduced average carcass size. This has had a number of knock-on effects for producers.

Smaller birds are understandably more expensive, per kilo, to produce. The feed and input price increases have made production even more expensive. Smaller birds have the advantage of permitting farmers to have more crops per year but even squeezing in an extra flock only helps offset input cost rises.

Rising input costs

Probably the single biggest influence on UK poultry farmers has been the volatility of the price of inputs – especially wheat (typically 60% of feed) and gas (most use liquid petroleum gas for heating). The UK poultry industry uses in excess of 6.2 million mt per annum of compound feed, in laying hen, broiler, turkey and breeder farming systems. In April 2011, feed price was an average of £298 per metric ton. This was a rise of 4.9% in just one month. Lower than the record prices seen last year, but still close to its historical high.

This has increased the pressure on producers to increase efficiencies by investing in technologies such as heat exchangers and biomass boilers for heating their chicken houses. In January 2011, UK farmers were achieving an average return of £74.84 per kilo, but by April this had fallen to £72.8, so any efficiency is welcome.

However, farmers trying to reduce their production costs can find themselves stuck in red tape instead. The NFU is currently lobbying the UK government on the issue of on-farm combustion of poultry litter.

This would allow producers to combust their own poultry litter to heat their houses and tick many boxes in terms of renewable energy and sustainability. However, poultry litter is currently classed as “waste” unless it is spread on land. Burning waste requires a cost-prohibitive licence under the Waste Incineration Directive.

Environmental credentials

Poultry meat is gaining profile in the UK as an environmentally responsible choice and an exceptionally efficient way to provide the protein needed to feed a growing population.

For example, a kilo of beef requires between 15,000 and 70,000 litres of water to get to the consumer, where as a kilo of chicken requires between 3,500-5,700 litres. The NFU is currently working with Newcastle University on a project to calculate the lifetime carbon footprint, lcf, for poultry meat and eggs. Back in 2007, Cranfield University calculated the lcf of a number of meats as part of a study looking at pork production. The comparison figures for poultry were spectacular, with around one tenth of the carbon emissions of pork (per kilo of meat).

High welfare options

Despite price pressures, consumers are keen to stick to their welfare principles where possible. Encouraged by various vocal celebrities, welfare has become high on the media agenda. An example is celebrity Hugh Fearnley-Wittingstall’s “Chicken-Out” campaign for the abolition of intensive rearing. As a result of this, and a long history of similar publicity, the majority of the public have extremely negative perceptions of intensive rearing methods. There is also a move by retailers to introduce certain perceived welfare aspects to their conventional chicken production, such as the addition of windows for natural light.

However, welfare is difficult to measure. The effects of a good stockman can be greater than most of the measures Mr Fearnley-Wittingstall and his compatriots are keen to promote. A relatively low stocking density of 28kg per m2 already forms part of the well-used “Red Tractor” scheme, used to identify responsible UK producers. This is well below the EU-imposed figure of 39kg per m2. However, it is important to remember that even free-range birds can suffer from extreme welfare problems when managed poorly.

Welfare is extremely high on the agenda of some of the country’s largest supermarket chains. Sainsbury says it aspires to be selling only higher welfare chicken by 2016. With the majority of financial pundits expecting an end to the UK’s austerity drive in about three years, maybe they are not too far off.