African producers accounted for 4% of world egg production in 2008 – a slight fall on their 1990 share. The region is not a major contributor to global trade nor production. You could be forgiven for thinking that this is a stagnant market, but, as Dr Hans-Wilhem Windorst’s report on the continent prepared for the International Egg Commission reveals, you would not be further from the truth.

World egg production grew by 72.4% from 35.2 million metric tons in 1990 to almost 61 million mt in 2008. Asia dominated production, with 58.8% of global output in 2008. By contrast, the African continent contributed 4.0% to global production volumes, a fall of 0.4% since 1990. African nations are not major egg traders either. Europe still leads the global egg trade with around two-thirds of total egg imports and exports.

But the overall picture hides a sector with dramatic changes in the period Dr Windhorst explains. Rising per capita consumption in a relatively small number of African nations has fuelled growth in the whole continent. This consumption growth was the direct result of greater buying power in several Northern and Southern African countries. In 2008, the three leading African producer nations -- Nigeria, South Africa and Egypt -- were responsible for 54.4% of the continent’s egg output.

Regional variety

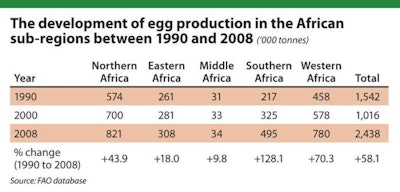

Dr Windhorst divides African nations into five regions. Each with quite different characteristics. Between 1990 and 2008, egg production in Africa as a whole grew from 1.5 million tonnes to 2.4 million tonnes (+58.1%). Only three of the sub-regions have shown any real growth – Southern Africa (+128.1%), Western Africa (+70.3%) and Northern Africa (43.9%). However, even within these sub-regions, there are dramatic variations between nations. Also, the regional concentration in most sub-regions is rather high. In most cases, only one or a very few countries dominate.

Northern and Western African countries contributed 33.7% 32.0% respectively of overall production volumes. Southern African countries shared 20.3% of production (albeit the vast majority being in South Africa). Eastern and Middle African nations combined contributed around 14.0% of output.

Northern Africa

Egypt, Morocco and Algeria dominate the area – with over 70% of egg production in 2008. There may have been growth in all of these nations from 1990 to 2008 but it was very uneven. In spite of high absolute growth, the contribution of Northern African countries to African egg production decreased in the analysed period because of higher growth rates in Southern and Western Africa.

Egyptian output actually fell between 1990 and 1992 before starting an upward trend – only interrupted in 1996 and 1999. The flat output from 2003 may represent missing data as a drop due to avian influenza seems likely during this period.

Moroccan output fluctuated considerably with a peak of 245,000 mt in 1999 followed by a decline to 168,000 mt in 2006. It is too early to tell if the recent upward trend is likely to be a real reversal in fortunes or a blip in a declining market.

Algerian production also showed a series of ups and downs – falling from 140,000 mt in 1990 to 85,000 mt between 1996 and 2001 before rising to a peak of 190,000 mt in 2007 and 2008.

The Tunisian egg market was much less volatile, with a general upward trend, broken only by slight falls in 1993 and 2004. Libya and Sudan showed similar patterns, although the production volumes are reportedly unchanged for the last eight years of data.

Western Africa

Nigeria dominates egg production in Western Africa. Not only is it the largest producer in the entire country, it produces more than ten-times the quantity of eggs of its closest sub-regional competitor, Burkina Faso.

Before the late 1990s, Nigeria showed a more or less steady increase, but political instability caused a fall between 1995 and 1997. The relative market sizes are closely related to the size of population. Nigeria had a 2009 population of 149.2 million compared with only 15.7 million in Burkina Faso.

Although small in absolute output, Nigeria’s regional neighbours have enjoyed some dramatic production increases. Senegal’s egg production more than doubled, rising by 227% to 36,000 tonnes from 1990 to 2008. Guinea grew by 178% to 22,000 mt and Ghana, by 155% to 26,000 mt.

Southern Africa

South Africa is not only the largest egg producing nation in the entire continent, it is the only country in the sub-region to be even placed within the top producers 20 globally. Part of the reason for the country’s dominance is its population of 50 million. However, its relative affluence and the comparatively large amount of people of European and Asian descent play a vital role too. In 2008, the country produced 485,000 tonnes of shell eggs, 273,000 mt more than in 1990.

Eastern Africa

Eastern African production grew by only 18% between 1990 and 2008. Unlike the other sub-regions, production is relatively evenly split between a number of countries. Kenya is largest, with production of 69,000 tonnes but six of its regional partners are also in Africa’s top 20 producers.

Looking more closely at the individual countries shows that, even though production volume increased in all of them between 1990 and 2008, the actual growth pattern varied considerably. Kenya showed an initial peak in late 1990s, followed by a sharp decline from 2002 which then became a general upward trend. Zambia is the only country in the sub-region to show almost uninterrupted growth. This may well be a reflection of its relative political stability.

Middle Africa

The Middle African region is only a relatively minor egg-producer, with no nations within the top 20. The largest producer is Cameroon, with only 14,000 mt output in 2008. The next highest, the Democratic Republic of Congo, has an average per capita consumption of only two eggs per year.

Trade deficit

Despite its relatively low per capita egg consumption, Africa had a trade deficit of almost 32,200 mt in 2007. The Middle African nations were the largest importers, buying in 16,700 mt of eggs. The only sub-region to have a positive trade balance was East Africa, with 777 mt.

It seems likely that African demand is going to continue to outstrip supply, despite some remarkable individual production growth figures. Dr Windhorst concludes that lack of capital, technical knowledge, growing political instability and low economic development status will prove to be the main inhibiting factors.