layers in South Africa decreased last year and further contraction is expected in 2014.

The contraction in South Africa’s egg industry is thought to have continued this year as the sector continues to confront weak consumer demand, volatile feed costs and rising labor costs.

Data published midyear by the Egg Organisation Committee of the South African Poultry Association (SAPA) suggests that output will shrink by 5.5 percent to 380,000 cases per week this year, after reasonably stable output of 402,011 cases per week in 2013, when gross production was worth ZAR8.6 billion (US$810 million).

The average layer flock is expected to decrease by a similar amount, falling by 5.2 percent, this year to 23.1 million head.

The current state of play is very different to the strong position South Africa’s egg farmers found themselves in a decade ago.

Difficult 10 years

In 2005-06, the South African egg industry was in the enviable position of being able to sell more eggs at higher prices -- the result of growing consumer demand fueled by high levels of disposable income. However, this was not to last.

In the latter half of 2006, egg prices started to fall, and producers took 12 months to cut back production. Just as the economic downturn was starting, the egg sector found itself still producing more than the market could absorb.

And despite weak market conditions, egg production rose in 2010 and again in 2011.

These increases coincided with higher feed ingredient and other input costs. Although the industry tried to increase prices to compensate for these higher costs, deteriorating market conditions meant producers’ efforts were largely unsuccessful.

Nevertheless, producers held on to some hope that both output and prices would improve by late 2013. These hopes, however, were not realized. Per capita egg consumption in South Africa contracted last year by 4 percent to 147.

High costs, weak demand, and oversupply have resulting in some South African producers leaving the egg sector altogether.

It has, however, been possible to pass some costs on, SAPA notes, but increases in egg prices at retail level are not necessarily feeding back to producers. For example, in 2008 the average retail mark-up on eggs stood at 49 percent. By 2013, this had climbed to 57 percent.

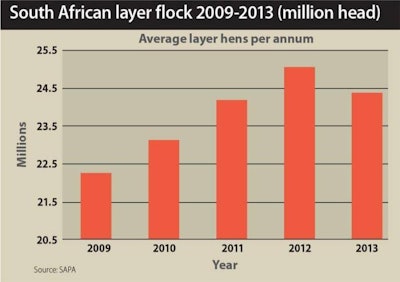

Smaller laying flock

Given ongoing market difficulties, it is not surprising that the number of birds farmed for eggs in South Africa has been declining.

Pullet placements started to register a gradual downturn mid-2011, and this has continued. This downturn, however, was forecast to have bottomed out by the middle of 2014, from which point a slight increase has been expected.

Over the first four months of 2014, the South African laying flock is thought to have contracted by 7.1 percent to 23.170 million, continuing the contraction that occurred in 2013 when it shrank by 0.7 percent. By year-end, the country’s laying flock is forecast to have contracted by 5.2 percent to stand at 1.3 million layers.