The world poultry production and profit forecast shows poultry profit margins weakening worldwide, after strong performance in 2014, but the forecast is for poultry margins to continue favorable in 2015 due to low grain prices.

Today’s positive global production forecast, in fact, means poultry producers around the world must answer the questions that come perennially in good economic times:

- Is there an overexpansion of world poultry production developing that will ruin the currently favorable economic forecast?

- When the next downturn in profitability occurs, will poultry companies be prepared with adequate capital reserves and the right business strategies?

Caveat with world poultry production forecasts

In an exclusive interview with WATT Global Media editors Gary Thornton and Mark Clements, poultry industry economist and consultant Gordon Butland discussed the production outlook for the global poultry industry, and the strategies of some of the world’s leading broiler chicken producers.

Butland issued a warning for poultry producers: Don’t be suckered by today’s economic headlines as you make business decisions for 2015 and beyond. Worldwide poultry production forecasts are complex and can be misleading when it comes to an individual poultry company’s outlook and markets.

Some poultry producers, perhaps overly influenced by the current favorable outlook, may be expanding too aggressively at this time, he said.

Poultry production forecast for 2015

Butland’s poultry production forecast and profit outlook is consistent with that of most industry experts – 2015 should be a profitable year with demand for poultry on the upswing and grain prices continuing to be favorable in many parts of the world – but he argues that poultry companies should assess their own market opportunities and exposure to risk in planning for 2015 and beyond.

He provided the following poultry production forecast for 2015 by world regions:

- U.S. poultry producers should experience profitable operations in 2015, as grain prices continue to be low, resulting in good margins. Demand for poultry should be stronger due to consumers' increased disposable income resulting from lower gasoline prices.

- Brazilian poultry producers will experience profitability, though the outlook is clouded by the possibility of overproduction and lower prices for chicken exports. A weak economy won’t help domestic consumption, but a weaker real may help exports.

- European poultry producers will benefit from lower grain prices and gasoline prices in 2015. Europe is becoming more self-sufficient in the production of poultry.

- Asian poultry producers are expected to have a difficult year due to overproduction and the presence of avian influenza in the region. Producers here are at a competitive disadvantage due to Asia's higher grain costs.

“The poultry outlook is not bad all over the world, and it’s not good over the entire world,” Butland said. “Poultry producers should guard against basing their planning on worldwide poultry production trends or even regional trends, but must include local and company-specific factors."

He suggested several questions that poultry producers should be asking themselves:

- Where are my markets growing now and in the future?

- If my markets are not growing, how can I take business away from competitors?

- How can my company become a low-cost competitor?

How the world’s leading poultry producers strategize

Leading poultry producers in Brazil and the U.S. see the need to get closer to consumer markets, Butland said. This is demonstrated in the business strategies of Tyson Foods and Brasil Foods.

“Key poultry companies are moving further out in the food supply chain to become food companies and not just primary processors of poultry,” he explained. “The earnings multiples for food companies are far superior to those of poultry companies focused on farming and processing.”

Tyson Foods pursues branded foods strategy

The purchase of branded foods company Hillshire Brands by Tyson Foods in 2014 is an example of a U.S.-based poultry producer-processor that has made the leap into branded foods.

“Tyson Foods is a much different company today than it was before the acquisition of Hillshire Brands. It appears the company is becoming more selective in the deployment of capital and the nature of the customers and business it pursues,” he said.

He cited Tyson’s divestiture of poultry operations in Mexico and Brazil as examples of the difference in the company’s business strategy.

“The acquisition of Hillshire Brands appears to have changed the dynamics completely at Tyson Foods,” he said. “It certainly can no longer be characterized as just a primary processor of red meats and chicken."

Brasil Foods follows international poultry strategy

Brasil Foods is another poultry producer that has articulated a strategy of becoming more of a food company, for which earnings multiples are higher, according to Butland.

In moves designed to rationalize business and improve profitability, Brasil Foods reportedly has reduced the number of SKUs and become more selective in the customers and markets served.

What’s more, Brasil Foods exploits an international footprint by producing poultry meat in Brazil (where live production costs are relatively low due to proximity to grains) and shipping the raw meat for further processing to operations elsewhere in the world that are close to available labor and consumers.

Competition in world poultry production getting tougher

Much of Butland’s poultry production forecast and analysis centered on the broiler chicken production industries in Brazil and the United States, the world’s leading poultry production industries and exporters.

He foresees overproduction of poultry in certain world regions and business sectors, as broiler chicken producers respond to profitable market conditions with expansions in supply.

One of those markets is Brazil, where Brasil Foods and JBS account for more than 50 percent of broiler chicken production and more than 70 percent of that industry’s exports. The Brazilian cooperatives account for another 10 percent to 15 percent of chicken production, he noted.

Butland considers broiler chicken producers in certain sectors of Brazil’s poultry industry as being vulnerable to poor profitably as increased supply materializes in coming months.

He observed that the smaller independent poultry production companies in Brazil are at a competitive disadvantage to the larger poultry firms, which have substantial capital reserves and international operations and market reach.

Poultry production forecast for Brazil

The Brazilian poultry industry is perhaps getting ahead of itself in production increases, Butland suggests, and this could lead to oversupply and lower margins.

He foresees the possibility of more poultry company acquisitions by major producers in Brazil as smaller competitors struggle to finance their companies and access markets with higher profit margins.

“The amount of new poultry production capacity going into production in Brazil is significant,” he said, and he believes some poultry producers there are too optimistic in their outlook and planning.

Weak economic growth in Brazil adds risk for producers

The forecast for weak poultry demand in Brazil due to anemic economic growth could heighten the economic squeeze on poultry industry competitors, if Butland is right in his economic assessment.

While U.S. consumer demand for poultry is forecast to improve with continued lower gasoline prices, this is not true in Brazil, where GDP might rise by no more than 1 percent in 2015, according to Butland’s projections.

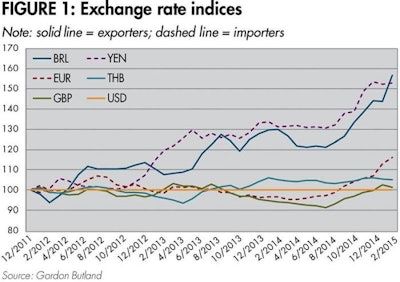

“In Brazil, the condition of the general economy has been a big question mark,” he said. “Whereas many regions of the world are benefiting from lower gasoline prices, this has not been the case in Brazil. Not only is the price of gasoline not going down, but other living expenses for people are increasing, including utilities. As a result, consumers in Brazil have less disposable income to buy poultry."

The combination of a weak general economy in Brazil and the forecast expansion in broiler chicken production is likely to weaken poultry industry profitability going forward, he said.

Competitive differentials exist in global production

Whatever an individual poultry producer’s size, a company’s geographic location, as it relates to grain costs and the availability of labor, as well as market strategy make a significant difference in the world poultry production competition and profit outlook, Butland said.

Geographic location can also play a major role in competitiveness in poultry production and in some cases renders generalizations less meaningful. The Brazilian state of Parana, for example, has the nation’s lowest broiler chicken production costs. Butland pointed to the R$3 (US$1.04) cost advantage per 60-kilogram sack of corn enjoyed by Parana poultry producers versus producers in the neighboring state of Santa Catarina.

Cost differentials exist for grains among the world’s poultry producers. The cost of corn is cheaper in Brazil than it is in Thailand, where the price is typically double.

While grain prices have fallen for poultry producers worldwide in the past year, poultry producers have paid more for logistics and shipping of grains everywhere, and more in some places in the world due to currency exchange rates. Corn prices, in fact, vary greatly in different regions of Brazil, and shipping costs can double prices in some areas.

Growing demand for automation in world poultry production

The availability of labor, or lack thereof, is affecting the competitiveness of poultry producers around the world, and there is a growing demand for automation, according to Butland.

“As poultry producers in Brazil, for example, think about increasing their productive capacity, they must consider the labor shortages that exist in many parts of the country,” he explained. “The demand for automation is up more so in Brazil than other places, but also in places where you might think there is no shortage of labor. So the demand for automation for the world’s poultry production and processing will remain strong for quite a long time."

Poultry companies investing in operational efficiency

Poultry companies around the world continue to invest in their operational efficiency, Butland said.

“Profitability for poultry producers in much of the world in 2013 was fantastic, and in 2014 was very good, and in 2015 will be reasonable for the industry overall,” he said.

He continued: “When poultry producers are making money, they invest in their operations because they are aware that they must become more efficient.”

“For example, there is quite a bit of investment occurring in hatchery operations because poultry companies recognize that while profitability has been good, they must remain competitive.

“Poultry producers for these reasons are in much better position today to weather any unfavorable economic conditions that might occur,” he concluded.