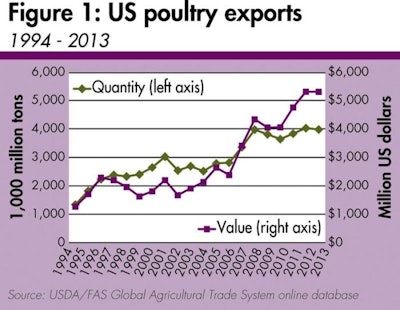

Broiler exports, which make up the bulk of the total, grew from 1.307 MMT in 1994 to 3.632 MMT in 2013 at an annual rate of 5.5 percent. Turkey exports, meanwhile, went from 30,771 metric tons (MT) in 1994 to 344,346 MT in 2013, increasing at an annual rate of 13.6 percent.

Will growth in U.S. poultry exports continue?

The question to be posed to the Magic 8-Ball is this: Can U.S. poultry exports continue to grow at this amazing rate for the next decade and beyond?

The Ball’s response: “All signs point to yes.”

USDA agrees. In its most recent long-term outlook, the Economic Research Service (ERS) projects that over the next 10 years (through 2023), U.S. poultry exports will continue to increase at an average rate of 1.4 percent. Although the economic model on which it bases its long-term projections is sound, ERS is somewhat conservative in its forecasts, according to Dr. Renan Zhuang, director of economic analysis at the USA Poultry & Egg Export Council (USAPEEC).

“We believe USDA’s projected growth rates tend to be conservative, based on projections from other sources and the market outcome for U.S. poultry exports over the past two decades,” Zhuang said. “According to the most recent long-term forecast conducted jointly by [the Organization for Economic Cooperation and Development (OECD)] and [the Food and Agriculture Organization of the UN (FAO)], U.S. poultry exports are projected to increase at an average annual rate of 2.7 percent through 2023.”

Poultry exports outpace production

Poultry export growth over the past two decades has outpaced increases in both chicken and turkey production and, as a result, the percentage of production that is exported has also increased. For broilers, the export share of production (by ready-to-cook weight) increased from 11.8 percent in 1994 to 20.8 percent in 2013, and for turkey the share of production exported rose from 5.7 percent to 13.1 percent.

Using historical data to formulate economic projections is rife with pitfalls, however. One need look no further than Russia’s sudden ban in August on imports of agricultural products (including poultry) from the U.S., the European Union, and several other countries to see that, just because an export market has been good over a long period doesn’t mean that it will remain so.

Diversification and new markets

One reason for optimism that steady growth in U.S. poultry exports will continue is the ability of the industry to seek out new markets in the face of adversity. In a recent analysis, Zhuang pointed out that exports have become more diversified. In 1994, the U.S. shipped 1.3 MMT of broiler meat to 80 countries, 73 percent of which went to the top five of those markets. By contrast, in 2013 U.S. shippers exported 3.6 MMT of broiler products to 118 countries and regions, with the top five markets accounting for 43.4 percent of the total.

This diversification effort by the industry, which USAPEEC has championed for years, has helped exports to continue to thrive despite multiple setbacks. Russia’s 1996 ban of U.S. poultry planted the seeds for market diversification. At the time, Russia was the top market for U.S. chicken, and accounted for more than 40 percent by volume of total U.S. chicken exports. The ban was a wake-up call for the industry, as prices for chicken leg quarters – the major poultry item exported to Russia and elsewhere – dropped by half virtually overnight. So much product was left on the market that some producers resorted to sending leg quarters to rendering.

Protectionism caused setbacks

Then, in 1997, the EU prohibited imports of poultry that had been rinsed in chlorinated water. Since most U.S. chicken and turkey slaughter plants use chlorine in the chiller as an effective anti-microbial treatment, the EU’s action slammed the door permanently on a market that at the time was valued at more than $50 million annually. Soon after, in 1999, South Africa launched an anti-dumping investigation against U.S. chicken, claiming that imports were causing economic injury to the domestic industry. Despite a vigorous (and expensive) defense, South African trade officials ruled against the U.S., and imposed high punitive duties that closed another valuable export market.

In 2009, the Chinese government initiated anti-dumping and countervailing duty investigations targeting U.S. poultry imports. As expected, China ruled in favor of its domestic industry, and imposed a range of duties from nearly 50 percent to 136 percent, which made exporting to China prohibitive. The U.S. took the case to the World Trade Organization (WTO), and although a WTO dispute settlement panel found in favor of the U.S., China has yet to revise the duties to an acceptable level.

The mounting series of protectionist challenges in key markets forced exporters to adapt and to exploit the competitive advantage of U.S. poultry in a global marketplace hungry for affordable protein. In his analysis on export diversification, Zhuang pointed out that from 1997 to 2013 the industry developed 31 new markets and reopened six for U.S. poultry. The 10 largest among them, by volume, are Cuba, Iraq, Turkmenistan, Congo, Libya, Kyrgyzstan, Sierra Leone, Tajikistan, Kosovo and Equatorial Guinea. Over that period, those markets accounted for more than 351,000 MT of product.

“Russia actually did us a favor,” said one longtime exporter who asked not to be named. “The Russians were busting our chops for years, and as we were exporting less and less to them, we were naturally being weaned. We've gone from essentially three major markets to many more.”

Five reasons for optimism about future exports

Zhuang’s analysis cites several reasons why the outlook for the next decade is bright:

- 1. Poultry is among the most efficient animal proteins. Production demands less water, uses less arable land, and emits less greenhouse gases than red meat, and is the most efficient converter of feed. Global poultry production and consumption will continue to increase as the importance of feed efficiency and protecting the environment become higher priorities for producing countries.

- 2. Consumer income will grow faster in developing countries. According to ERS, per capita real GDP in developing countries is projected to grow at an average annual rate of 4.2 percent through 2023, while that in developed countries is predicted to be about 1.7 percent. Higher income in developing countries will lead to higher protein consumption, particularly poultry, as annual per capita poultry consumption in developing countries is generally much lower than in developed countries. For example, per capita chicken consumption in China is under 10 kilograms and is 3 kilograms in India, compared to more than 42 kilograms in the U.S.

- 3. Over the next 10 years, the average annual global population increase is predicted to be 74 million. Population in developed countries is projected to grow at an average annual rate of 0.4 percent, while population in developing countries is predicted to increase at an average annual rate of 1.2 percent. Increasing Islamic populations will favor poultry consumption.

- 4. Domestic demand for poultry in most developing countries is expected to increase at a faster pace than domestic production. In many developing countries and regions (China, the Middle East and Sub-Saharan Africa), production will continue to be constrained for the foreseeable future by the scarcity of water and dependence on imported feed grains, which will drive demand for imports.

- 5. Urbanization and westernization of food in developing countries will also help to boost consumption of poultry meat. In the past five years, the number of KFC restaurants in China increased from 2,872 to 4,563, an average annual growth rate of 12 percent. During the same period in India, the number of KFC restaurants increased at an annual rate of 36 percent. China now has more KFC outlets than the U.S.

Competitive picture for U.S. exports

Although the U.S. and Brazil will continue to be the dominant players over the next 10 years – together, they account for two-thirds of global trade in poultry – the two heavyweights rarely compete head-to-head. U.S. chicken exports are mainly leg quarters, while Brazil with its lower (but rising) labor costs exports more specialized further processed products, including small whole-bird grillers that are popular in the Middle East.

The U.S., of course, will continue to be the world’s major producer and exporter of turkey meat, mainly in the form of mechanically separated turkey that is in high demand as an ingredient in meat processing worldwide. The U.S. has an insurmountable edge over all other suppliers in Mexico, which accounts for half of all U.S. turkey exports, because product can be trucked fresh to the border in two days from virtually any state where it is produced. Even though Brazil and Chile have made some inroads in shipping turkey to Mexico, it is difficult for frozen product to compete with chilled.

The overall competitiveness of U.S. poultry exports in the world market will remain strong in the next decade as the U.S. has a low-cost and high-quality feed supply, good biosecurity practices, consistent and stable government regulation, and growing global demand for low-cost chicken cuts and turkey products.