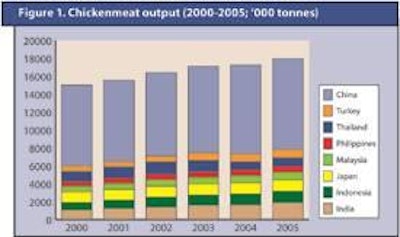

The fastest growing chicken meat industry in Asia – if not the world – is India, where annual output has jumped from just under 1.1 million tonnes (mt) in 2000 to an estimated 1.9mt in 2005. An outbreak of highly pathogenic avian influenza (HPAI) early in 2006 will likely mean that output will not exceed 2.0mt this year but, assuming no more outbreaks, then at least one forecast points to Indian broiler production reaching 2.2mt in 2007. A long-range forecast by the USA’s Food and Agricultural Policy Research Institute (FAPRI) points to this figure rising to around 2.8mt by 2015. This expansion reflects continued strong growth in domestic demand in response to affordable prices and increasing incomes. Integrated operations have expanded their share of production and this has given rise to improved liveweight at slaughter and dressed yield.

Poultrymeat is now the major meat eaten in this country, with the average quantity estimated at 1.9kg/person in 2006.

According to a USDA Gain report, “Expanding domestic production and increasing integration have pushed poultrymeat prices downwards and stimulated consumption. The integrators have established price leadership in their markets by reducing the number of middlemen and forcing wholesalers and retailers to cut their margins.”

However, the majority of Indians still prefer fresh chicken, often slaughtered at small corner shops. Some integrators are marketing branded chilled chicken products at retail level but, in general, the market for processed poultrymeat is constrained by inadequate cold-chain facilities and the consumer preference for fresh meat.

Indonesia

In most Asian countries, it is difficult to put a figure on the production of meat from village flocks. However, FAO figures indicate that total annual chicken meat output in Indonesia is now around 1.3mt. Data from another source point to a broilermeat output in 2006 of a little under 0.7mt while the forecast for 2007 is some 0.72mt and by 2015, it could be in the region of 0.9mt

Around 80% of birds are sold in traditional wet markets as Indonesians tends to prefer freshly slaughtered chicken. Some 19 integrated processing plants handle the remaining 20%, tending to supply food manufacturers, food service industries and supermarkets.

Avian influenza is endemic. Backyard poultry are an income-generating activity for people in rural areas and the success of the culling of poultry surrounding an outbreak is greatly dependent on the compensation offered by the government. To date, this has been viewed as inadequate, which might have led to delays in the reporting of the disease.

Day-old chick production for broilers in 2006 is forecast at approximately 17 million/week or 880 million/year and is expected to total around 925m next year. Industry capacity is put at 26 million/week.

For the country’s 222 million people, broiler consumption is assessed at 3.1kg/year – well below that of many neighbouring countries. The development of this sector has been greatly influenced by the production of nuggets and sausages that make meat more affordable.

Japan

Chicken meat production in Japan has shown negligible growth at around the 1.2-1.3mt mark. The medium-term forecasts indicate no significant change. The market has been over-supplied. With total consumption expected to grow only marginally, a cutback in production will be required if a recovery in chicken meat prices is to occur. A continued surplus is expected to limit import growth of processed and cooked chicken products while creating increased competition between Thailand and China in the food service and ready-to-eat markets.

Total broilermeat consumption in 2007 is anticipated to increase slightly to 1.92mt, with the uptake of unprocessed broilermeat unchanged at 1.57mt and that of imported and prepared processed products up by just 1% to 0.35mt. Total imports are expected to decline by 3% to 725,000t with purchases of the unprocessed product down by 5% to 380,000t, while receipts of prepared and processed chicken products are forecast unchanged at 345,000t. Prepared and processed products currently represent around 48% of total imports, and it is anticipated that this quantity and proportion will continue to grow in the foreseeable future. The long-term view is for a slight reduction in domestic production offset by an increase in imports.

Malaysia

With average chicken meat consumption in the region of 35kg/person/year, Malaysia has one of the highest rates in the world. Production has trended upwards since 2000 to the latest figure released by the FAO of 860,000t for 2005. The forecast for 2006 is over 900,000t.

In 2005, day-old broiler chick production was assessed at 462 million and projected to reach 480m in 2006. Integrated operations accounted for 62% of this total.

Only some 30% of broilers are handled by modern processing plants as most birds are sold live or dressed at wet markets. Outbreaks of H5N1 were tackled in 2004 and 2006, and the country was declared free of the disease on 21 June 2006.

A robust further-processing industry has been developed. Chicken frankfurters, cocktail sausages, burgers and nuggets, which in the past were exclusively imported, are now produced locally.

The Philippines

The country aims to become a ‘halal food hub’ and is well positioned to supply halal poultry to other Islamic countries and Muslim consumers worldwide.

Chicken meat production in the Philippines, according to the Bureau of Agricultural Statistics (BAS) amounted to 1.22mt liveweight in 2005. The BAS estimates that broilers account for about 62% of this total, with native chicken providing 13% and meat from culled layers 2%. The remaining 23% is considered to comprise other chicken including what are described as ‘roosters’. On this basis, the data provided by the FAO in the accompanying table would represent only a little more than the broilermeat sector. By 2015, FAPRI forecasts that broiler production in the Philippines will reach 814,000t.

Four major integrators are thought to meet about 65% of total demand. According to the University of Asia and the Pacific, the market divides into two distinct product preferences: the fast-food chains require volume delivery, mainly marinated parts, and are particular about specifications, value, quality and reliability, while hotels, restaurants and other institutional buyers require whole chickens and have a more variable pricing policy compared with the relatively stable prices of the fast-food outlets.

Wet markets provide the majority of daily household requirements, offering whole birds and parts. There is a growing trend for householders to buy from supermarkets. Currently, such stores supply around 10% of the retail trade in chicken. As only about 10% of households have a refrigerator, fresh meats have to be cooked soon after purchase.

Thailand

According to a USDA Gain report, chicken consumption slipped a little in 2005 to 7.85kg/person from the previous year’s 8.26kg, reflecting weaker consumer purchasing power as a result of higher retail prices and the imposition of new taxes.

Broiler industry developments in Thailand have to a great extent been dependent on continued growth in exports. However, as shipments to the EU and Japan have been limited over the past few years, the expansion of the broiler sector has been driven by domestic consumption. Although output has shown signs of recovering, the estimate of around 1.1mt for 2007 will still fail to match the 2002 record of 1.32mt. FAPRI forecasts that broiler production will reach 1.71mt by 2015.

When the media reported on the re-appearance of HPAI and related human deaths in late July 2006, poultry consumption slumped, and uptake in August and September was as much as 20-25% below the June level. However, over the year, domestic broiler consumption at around 770,000t could still exceed the 2005 figure of 730,000t. The forecast for 2007 points to a further increase to 810,000t.

After showing positive growth over the first half of 2006, the export outlook for the second half of the year became less optimistic following the European Union decision to extend the ban on raw poultry products from Thailand and the imposition of a new import system on poultry products. In addition, there were signs of a lack of growth in the Japanese market. During the first half of 2006, Japan purchased 53% of Thai’s total exports by volume, while the EU accounted for 42%. Nevertheless, total trade for the year could reach 280,000t but this figure is unlikely to be surpassed in 2007.

Turkey

Poultrymeat and egg consumption were badly hit by the outbreak of HPAI in Turkey. At one stage, uptake was 30 to 40% down on 2005 levels. While the optimists are looking for broiler production in 2006 to match the latest figure for 2005 of around 960,000t, others take the view that it could be some 10% lower.

Egg production

With an annual total of 35.75mt, Asia accounts for 60% of world hen egg production. As can be seen from Table 4, China is responsible for some 68% of the Asian total. Excluding China, then in 2005, India took over from Japan as the leading egg producing nation in this region with an annual output of close to 2.5mt.

Estimates for 2006 were not available at the time of going to press but there can be little doubt that the effects of the outbreaks of HPAI on production and demand will have impacted adversely on total output in most countries in the region. Indeed, one report to hand on Turkey indicates that in mid-2006, the commercial laying flock was estimated at around 34 million (including eight million replacement birds) compared with 43m (including 14m replacements) in the previous year.