Brazil has lost its place as the cheapest location in the world to produce pigs. That was the startling declaration by a speaker at a congress in Cuiabá, Brazil, earlier this year. Our production costs used to be in the range of US$0.50-0.70 per kilogram, he went on. But with the US dollar weakening and the Brazilian Real strengthening, we are now somewhere around US$1.30 or about double the traditional figure.

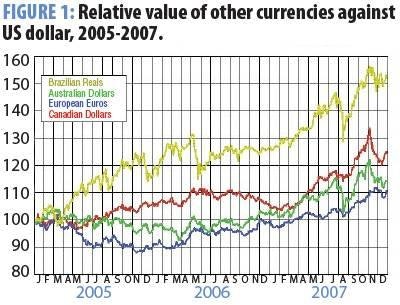

His remarks illustrated how currency exchange rates influence any attempt at comparing pig production costs on an international basis. See in Figure 1 the fluctuations that have affected the relative values of the major trading currencies in the past year. Even bearing these effects in mind, however, a special survey for this issue of Pig International seems to agree that Brazil can no longer claim to be undisputed as the world's cheapest producer of pork. Although local estimates have been converted to Euros in each case and that could lead to some distortion, whether the currency of comparison is the Euro or the US dollar does not alter the appearance that the USA, Mexico and Chile all have lower costs currently than southern Brazil.

A second outcome from our survey has been its illustration of the way in which rising feed grain prices have drastically changed production economics worldwide. For example, an examination of cost data for enterprises in the main pig-producing area of Germany in January 2008 has concluded that each slaughter pig for sale at 119kg would have cost some €175.44 to produce on a well organised farrow-to-finish unit. That worked out at €1.86 per kilogram deadweight. A year earlier, the cost of production at the same enterprise had been €133.93 per pig or €1.42 per kilo.

Effect of feed prices

An increase of 31% in the production cost in the space of just one year has found echoes in other countries around the world, according to the survey. Just as the Germans of Nordrhein-Westfalia now need about 40 Euro cents more per kilogram carcase weight than a year ago in order to break even, the Spanish producers of Cataluña have required some 21 cents. Their cost is reported to have increased by 16% between January 2007 and January 2008. One source in Spain suggests €1.07 per kilogram liveweight as the current all-costs count (including slurry disposal) for a well-run family farm of about 1000 sows — provided it is not new so it has very low amortisation or depreciation charges on its buildings. He proposes a killing-out percentage of 78% in this instance to convert to a cost per kilo deadweight, indicating some €1.37/kg carcase. Another Spanish source says cost levels were around €1.04 per kilogram bodyweight a year ago, rising to €1.20 in January 2008.

Italy gives a further example from Europe, even if its elevated slaughter weight does not allow Italian costs per kilo to be compared directly with those of other European producers. An upper-tier pork production enterprise in northern Italy is reckoned to have faced 17% higher total costs in January than a year earlier. Again the quotation is given on a liveweight basis, from €1.28/kg in January 2007 to €1.50/kg in January 2008. The source's own pigs sold at 165kg have a killing-out of 80-81%.

Our data search confirmed that the feed price impact has been global and not just European or North American, such as when we received estimates from Asia for each country's percentage increase in pig production cost between January 2007 and January 2008. Among these, the cost rise in Australia was suggested to have been 14%, in Thailand 15% and in China 22%.

In the Midwestern states of the USA the budget for complete feed at a major operator stayed around US$154 per metric ton in each of the 4 years 2003-2006, but rose to US$220 in 2007. For 2008, it is budgeted as US$286 per ton. After increasing 58% from 2006 to 2007, the average maize price is thought likely this year to work out another 34% higher at around US$5.10 per bushel. This year's January production cost of about 59 US cents per pound liveweight has meant losing over US$36 per pig.

Productive producers

The judgement on costs for producing each kilogram and therefore competitiveness must depend on the productivity performance of the unit, of course. In Russia, too, we are advised the one-year increase in feed raw material prices has been on the order of 15%. But good production figures are being recorded for Russian enterprises, some modern ones achieving in excess of 25 piglets weaned per sow/year. This has limited their total cost to 53-55 roubles, around 35-38 roubles of which is for feed depending on the cost per ton and feed conversion efficiency. On early-2008 rates of foreign exchange this would imply feed representing €0.98-1.06 out of a total of €1.48-1.53.

As we observed earlier, currency exchange rates can colour between-country comparisons. In receiving data about the Philippines, we were advised to assume a rate of 41 Philippine pesos per US dollar or approximately 59 pesos per Euro. On that basis a slaughter pig sold at around 90 kilograms this year has cost better producers some US$1.50/kg or €1.04/kg liveweight when the farmgate price has been about US$2/kg. But the backyard sector still constitutes roughly 75% of the national inventory of 14 million pigs. For backyarders, the estimated production cost recently was equal to US$1.66/kg or €1.15/kg liveweight. In the local currency the all-round increase has been from 83.3 pesos/kg carcase in January 2007 to 89.7 pesos/kg in January 2008. Also worth noting, says one source, is that pork carcases in the Philippines have been selling at the equivalent of US$3.90/kg.

Hungary's Research Institute of Agrar-Economy has produced an account of past costs with forecasts for how these might develop over the next 2-3 years. The report currency is Hungarian forints, with the cost per kilo carcase weight given as rising from HUF253 in 2003 and HUF264 in 2004, to HUF267 in 2005 and HUF277 in 2006. The indication for 2007 is HUF281 or approximately €1.06/kg.

In 2008 this is expected to become HUF287 or €1.08, although that seems low.

Also among the newer of the European Union's member states, Lithuania has an example of a farrow-to-finish herd with 3600 sows that buys feed in 2008 at 800 Lithuanian Litas (approximately €231) per ton. Feed accounts for 62.5% of the total production cost per kilogram liveweight of LtL3.8 or €1.11. Notably, labour and veterinary charges are each considered to represent about 9% of this amount, with social insurance adding 2.8%. Amortisation gives 4.2% and electricity 3.8%.

Farmgate prices slow to rise

The contrast between rising costs and near-flat pig prices is mentioned to us repeatedly. From France, the assessment by Inaporc for January 2008 was that slaughter pigs were costing some €1.58/kg to produce and yet the market was paying a base price of €1.06/kg, or around €1.18/kg with bonuses. In Ireland there are unofficial estimates that about 8000 sows or 5% of the national herd have been lost in the past 6-8 months due to the financial squeeze. Per kilogram of pigmeat produced, feed alone in January 2008 was costing the better Irish producers €1.16 and non-feed expenses added 0.48 so the total was up to €1.64, against a pig price of €1.38. In January 2007 Ireland's feed cost had been €0.88 and other costs €0.44, for a total of €1.32, while the pig price was €1.41/kg.

An increase of feed costs of about 20% in little more than 6 months and also a decrease of pig prices have been quoted to us by a source in the Netherlands when referring to Dutch margins. Put against figures from an annual survey showing what had already happened to Netherlands production costs in the period from July 2006 to June 2007, the increased price of feeds are indicated to have meant a negative margin recently even for Top-20 piglet producers and finishing unit operators.

Take a Dutch herd in the size range 400-450 sows and reckon it is in the top tier on physical results. Financially, on the costings from the national survey, such a unit probably could have made a profit of around €84 per sow/year in the 12 months to June 2007. The latest calculation with more expensive feeds is a loss of €245 per sow/year for the same establishment. A unit in the Netherlands with around 2900 finishing pigs is shown staying in profit by some €31 per finishing place per year until mid-2007, whereas now it is likely losing €12.75.

Actual numbers from the Dutch survey have been supplemented by expert local estimations of labour cost and depreciation to arrive at these conclusions, based on standard current labour rates for the unit's employees and 2008 prices for buildings.

Importance of location

Remember, though, that the location of an enterprise within a country can often make a difference to its comparative costs. Figures for Canada would need ideally to be sub-divided into eastern and western regions, with the prairie producers about C$12 per pig lower on costs than the C$152 reported at the end of last year for Ontario. Producers in Brazil agree there is a large difference in production costs from one state to another, particularly in different regions of the country.

The three southern Brazilian states which probably supply 90% of national production and 95% or more of pork exports are similar to each other on costs and prices. Of these, the participation by Paraná (PR) is relatively small so the focus tends to be on Rio Grande do Sul (RS) and Santa Catarina (SC) which together provide 80-85% of exports. Elsewhere in Brazil, São Paulo gives a contrast because almost all of its output is for small meat companies in the local market; also its feed costs are much higher than those in the south. The states in the north-east similarly produce only for local consumption and not for export. They have high costs, high prices.

With Brazilian cost data, therefore, the concentration is usually on the pigs aimed for the international market and that means using an average of either two (RS, SC) or three (RS, SC, PR) southern states. Government agricultural research organisation Embrapa surveys pig production costs. In its report for the 10 months January to October 2007 it pointed to a two-state average production cost of R$1.937 per kg and a three-state average of R$1.858/kg. At an annualised exchange rate of R$1.85 to the US dollar or R$2.64 per Euro these per-kilo amounts in Reals would become US$1.05 or €0.73 and US$1.00 or €0.70 respectively.

Average 2-state and 3-state prices during that time were R$1.748 and R$1.732 per kg liveweight, when an 8% bonus was added. A weekly survey of independent pig prices in Rio Grande do Sul during 2007 shows an average of R$1.95. In other words, at most times the producers in the southern states were seeing a loss of some 12-18 US cents per kilogram. Santa Catarina was worse because it had much lower prices during the year as a result of being unable to export pork to Russia.As everywhere, feed has been the main variable for RS costs during the last half year. According to Embrapa´s figures, the RS feed cost/kg started rising in September last year at a rate of about 6 cents per month, reaching R$1.587 by October. Similar increases have followed in November to January as both maize and soya prices continued rising. That has meant a January 2008 feed cost in Rio Grande do Sul up to R$1.77/kg. January's total costs were around R$2.42. Maize by that time had reached R$34 per 60kg bag or the equivalent of 31 US cents per kilo, twice what it cost in early 2007. Fortunately, there has since been a reduction because the main corn harvest came in during February. But the rise had already succeeded in denting Brazil's claimed place as the world's cheapest pork producer. PIGI