U.S. broiler exports are forecast to drop by 11 percent in 2015 due to the outbreaks of highly pathogenic avian influenza (HPAI) in 20 states, according to Will Sawyer, vice president with Rabobank’s food and agriculture research group.

Sawyer presented the forecast for U.S. chicken export volumes in the webinar, “Avian influenza: Control efforts and trade impacts,” presented by WATT Global Media and sponsored by Zoetis.

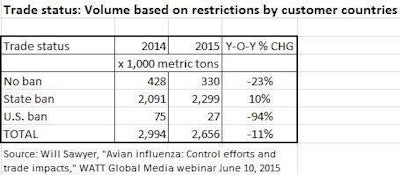

Rabobank’s surprisingly positive forecast is based on a complicated export landscape for U.S. poultry. While trade restrictions by the countries imposing U.S.-wide bans of chicken have cut into total U.S. exports, the countries banning chicken on a state-by-state basis are buying more U.S. chicken for now.

Texas is a key state for U.S. chicken trade

Sawyer’s forecast, however, assumes there will be no HPAI outbreaks in U.S. states not already affected by avian influenza, and there is significant risk in the trade situation. Texas, for example, is a key state where trade risk is involved.

“Texas is a primary productions state for broilers but also the key state of transit for broiler trade into Mexico,” Sawyer said. “Over 90 percent of the volume of U.S. chicken exports from the U.S. to Mexico goes by truck through Texas. Texas is the key to that trade continuing for the rest of 2015 and 2016."

“As this issue evolves over the next six to 12 months, we must watch the movement of AI across the U.S. and also the seasonal pattern of migratory birds to provide an indication of the trade impacts in 2016,” he said.

Low chicken leg quarter prices driving demand

The U.S. broiler industry’s work to diversify its export markets is paying dividends in the current disease crisis, Sawyer said.

While U.S. chicken exports to countries that have banned U.S. poultry in its entirety are expected to drop to near zero for the remainder of 2015, countries like Taiwan, Hong Kong and Vietnam, which are taking a state-by-state approach to bans, have significantly increased their volumes of imported U.S. chicken, he said.

The relatively low price of U.S. leg quarters is a key factor driving the trade in Canada, Mexico and parts of Southeast Asia, he explained.

He also indicated that some countries in Southeast Asia may be acting as conduit for the shipment of U.S. leg quarters into countries that have imposed countrywide bans on U.S. poultry.

Risk of still lower chicken leg quarter prices

“While there has been a significant decline in leg quarter values on a cents-per-pound basis over the last 12 months – with leg quarter values going from 50 cents a pound to now closer to the low 30-cent-a-pound levels – leg quarter prices are still higher than the historic lows of the last 15 years,” Sawyer said.

“The risk is that avian influenza may expand into other important production states and more states would no longer be able to export into as many markets,” he continued.

Leg quarter prices could decline further in such a case, he said, “but we see a bottom in leg quarter prices in the high teens, if this should occur,” he said.

Strong U.S. demand for chicken buoys market

Meanwhile, profitability of U.S. broiler companies in North America remains historically high. This is driven by strong domestic demand and relatively low feed prices.

“As long as the U.S. consumer continues to pay reasonably high prices for chicken white meat, broiler producers in the U.S. should be able to weather what could be a significant trade impact from the avian influenza outbreaks better than might have been the case at other times,” Sawyer said.